Tweet

Tweet

Economic performance of India and Pakistan

By M. Osman Ghani

Indian economy was characterized as inward-looking, having low growth and higher poverty levels prior to 1991 balance of payment crisis. Real GDP growth averaged around 3.5 per cent per annum during 1951-80.

A well known Indian economist Raj Krishna's termed this type of growth as the "Hindu rate of growth" and it became part of economic diction. India's balance-of-payments crisis in 1991 followed an acceleration in economic growth to 5.6 per cent a year.

Low growth rate of 3.5 per cent over three decades and large fiscal deficits fed into current account deficits and depleted foreign exchange reserves, pushed India to the brink of default in 1991.

The general government fiscal deficit (centre and states consolidated) averaged 9 per cent of GDP before the crisis. The overall budget deficit rose from around 7 in 1997-98 to more than 10 per cent in 2002-03, due to a significant increase in government consumption and continued low revenue mobilization.

Persistence of large fiscal deficit resulted in accumulation of domestic debt beyond sustainable levels. The combined domestic debt-to-GDP ratio rose from about 58 in 1985-86 to 85 per cent of GDP in 2002-03 with contingent liabilities from loss-making public enterprises adding another 12 per cent of GDP.

In fact, the domestic debt-to-GDP ratio has accelerated from less than 2 per centage points of GDP per year over the first three years of the 9th Plan period (1997-98 to 1999-00) to more than 4.5 per centage points over the last three years (2000-01 to 2002-03), despite the low interest rates.

Besides this rise in the debt burden, the deteriorating quality of the fiscal stance in the 1990s has been a matter of serious concern for economic managers. Revenues fell considerably during the Ninth Plan period (1997-98 to 2001-02) relative to the second half of the 1980s. Compared with the average for the second half of the 1980s, capital expenditure fell by more than three percentage points of GDP during the Ninth Plan period.

India had no alternative but to seek assistance from the IMF under the Standby Arrangement which it had resisted for too long. In the process, India had to change its development strategy, which they followed for the last 40 years.

The new strategy is a mix of "loose fiscal-tight money" policy that has helped to keep inflation low and prevent worsening public debt dynamics from spilling over into the current account and depleting reserves, as happened in the late 1980s, leading to the 1991 crisis. But this has been at the expense of growth and welfare, as rising interest payments crowded out spending on social and physical infrastructure.

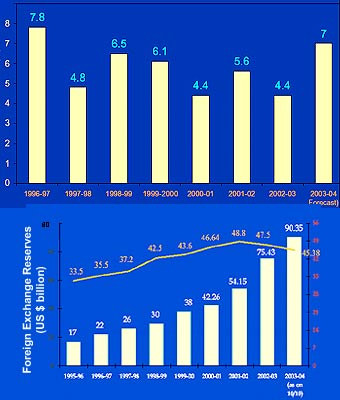

After remaining dormant for four decades, the Indian economy had picked growth momentum in the first half of the 1990s following the policies implemented in response to the 1991 crisis. However, compared with an average growth of around 6 percent through the 1990s, GDP growth decelerated to an average of 5.0 per cent in 1999-2000 and 2000-01 and is now estimated to have further declined to 4.4 per cent in FY2002-03.

There were many factors that have played important roles in depressing Indian economic growth including poor agricultural performance; ill-effects of economic sanctions following the nuclear tests; the hardening of international oil prices from $9.2 per barrel to $37.0 per barrel; meltdown of IT sector; tehelka.com's video-taped revelation about corruption in defence establishment and bankruptcy threats for Unit Trust of India (UTI) the largest mutual fund further eroded investor sentiments; and the persistence of large and unsustainable fiscal deficit (11 percent of GDP) causing public sector debt exceeding 85 percent of GDP. More importantly, the first generation of reforms launched in the early 1990s (after the 1991 balance of payments crisis) appear to have run out of fuel.

The slowdown during the late 1990s was broad-based across sectors, particularly in the agriculture and industry. Agricultural growth slowed to an average of 1.3 percent during last three years from an average of 4.75 percent in the mid-1990s - less than one-third the rate in the mid 1990s - and manufacturing sector growth slowed to an average of 3.8 percent as against 7.5 per cent in the mid 1990s - less than half the rate in the mid 1990s. The slowdown in growth was accompanied by a slowdown in investment, especially in the private sector.

Firms borrowed and invested heavily in the mid-1990s, building capacity for demand from continuing high growth rates and continuing reforms that would have surely generated high returns. Private sector investment growth plummeted to an average of only 3.75 as against an average of 15.2 per cent in the mid 1990s.

Higher public debt and higher interest rates also added to the debt service burden. As a result, resources available for public investment became tighter, with consequences for infrastructure development. The share of public sector investment in GDP declined from 11.2 in 1985-86 to 8.2 in 1992-93 and further to 6.6 per cent in 1997-98, and has now settled at 6.3 per cent of GDP in 2002-03.

The continued deterioration in fiscal balance and the associated rise in public debt along with slowdown in structural reforms are the key factors responsible for the deceleration in growth momentum in India. Given the size and depth of poverty in India, achieving annual growth of 8 per cent per annum is considered necessary to significantly reduce poverty in 5-10 year period.

It is in this context that recent deceleration of growth has emerged as a major source of concern. Notwithstanding the progress in poverty reduction in the past decade, some 400 million people (or 40 per cent of the population) still live on less than $1 a day, compared with 31 percent in Pakistan with same definition.

To look at the overall socio economic conditions of India there are other important criteria as well. More than 2.5 million people sleep on the footpath, and pavement in two major Indian cities only, namely Kolkata and Mumbai.

Anecdote like "millions of poor Indians born and die on footpaths" is not an exaggerated statement indeed. According to the WHO Report India is the second most AIDS-affected country in the world after South Africa, where up to 5 per cent of the population is already AIDS-infected or highly vulnerable to that fatal disease.

According to a recent statement of Indian Home Minister presently 165 separatist groups are actively engaged in secessionist activities in the nook and corner of the country, including 107 groups in the resources rich north eastern provinces. Communal violence's are on the rise. Minorities including Muslims, Christians and Untouchables are frequently subjected to arson and killings and wanton destruction of their property.

Violence and social disharmony, if not controlled may eat up whatever India has gain in her economic sector in the last few years. A comparison of economic performance of Pakistan and India during the outgoing fiscal year 2002-03 reveals interesting facts. [See Table-1]. It is evident that Pakistan is far better placed and reached a position of macroeconomic stability in recent years.

The fiscal space after long journey of fiscal prudence has finally attained and Pakistan can accelerate pace of social economic development faster than any other country in the region including India. Pakistan's per capita income has already increased from $420 in 2001 to $492 in 2003.

Pakistan has already achieved primary fiscal surplus and revenue deficit is near elimination which has helped Pakistan to improve its debt dynamics.

On the other hand the sharp increase in revenue deficits, which doubled from less than 3 per cent in the late 1980s to more than 6 per cent of GDP over the past six years, is a matter of serious concern for Indian economic managers.

Falling revenues-and rising expenditures have crowded out development spending, with negative implications for long-run growth and welfare. Growing interest payments have crowded out public investment, and high real interest rates have constrained private investment. Even though interest rates have declined over the past 18 months, public debt dynamics have continued to worsen.

Pakistan's exports are growing at a faster pace than India. Revenue collection in Pakistan has substantially improved during last three years while in India these are deteriorating. On the other hand Pakistan has not only succeeded in arresting increasing debt burden but domestic debt to GDP ratio has improved from 52.6 in 1999-2000 to 4 per cent in 2002-03.

This is because of the fact that Pakistan is able to lower fiscal deficit at around 4.5 per cent in 2002-03 while fiscal deficit in India has risen to double digit at 11 per cent of GDP. There was an across-the-board deterioration of fiscal indicators during the 9th Plan relative to the second half of the 1980s and an even more striking deterioration is to follow in the years to come. Table-1:

Many intellectuals in Pakistan are impressed with the impressive growth performance of India during 1990s but they must look into quality of growth. Pakistan had higher economic growth in the 1980s but fiscal deficit was left unbridled which had given rise to serious macroeconomic crisis in the 1990s.

Same is happening in India where fiscal stimulus is seen as desirable to counter the slowdown in private sector activity. But the arguments for a fiscal stimulus is not convincing when public debt levels are rising at such a brisk pace.

India's large fiscal imbalances pose a serious threat to sustained growth and development over the medium term. The persistence of current fiscal trends will, at best, limit growth and job creation. And slower growth would, in turn, speed the deterioration in debt dynamics.

If this negative cycle continues, a full-fledged fiscal crisis cannot be ruled out. On the surface, these fiscal indicators are worse than those faced in 1991-and worse than in many other countries that actually suffered a macroeconomic crisis. But the risk of crisis in India today is mitigated by the country's strong foreign exchange reserves. These reserves are able to finance 11 months of imports while Pakistan maintains reserve level of sufficiency for 12 months imports.

India has added about $22 billion during the past fiscal year, about 40 per cent of it after November 2002. An unknown part of this might have been driven by capital inflows related to fears of the Iraq war, so "this pace might not be maintained" (Reserve Bank of India 2003 report).

Without a fiscal adjustment, the growth even at 8 percent would be substandard. In other words, growth could continue to be substandard even if a crisis does not erupt-and avoiding crisis is not enough for India in present fiscal situation.

Major challenges for India in the near term are; first generation reform running out of fuel, fiscal responsibility and budget restraint law, continuing regional tension, communal violence, unsustainable fiscal deficit, growing subsidy and contingent liabilities, rising public debt, crowing out of private sector, economic growth slowing, likely setback on poverty front.

Table-1: Pakistan and India

A comparison of economic performance of 2002-03

Pakistan India

Real GDP growth (%) 5.1 4.3

Industrial growth (%) 8.6 5.8

Inflation (% growth in CPI) 3.1 4.0

Revenue (% of GDP) 17.6 18.4

Expenditure (% of GDP) 22.2 28.8

Fiscal deficit (% of GDP) 4.6 10.4

Revenue deficit (% of GDP) 0.5 6.9

Primary balance (% of GDP) 0.4 -3.8

Current account deficit (% of GDP) 4.8 0.7

Domestic debt (% of GDP) 46.0 85.0

Export growth (%) 22.0 19.2

Link:

http://www.dawn.com/2003/11/03/ebr11.htm

By M. Osman Ghani

Indian economy was characterized as inward-looking, having low growth and higher poverty levels prior to 1991 balance of payment crisis. Real GDP growth averaged around 3.5 per cent per annum during 1951-80.

A well known Indian economist Raj Krishna's termed this type of growth as the "Hindu rate of growth" and it became part of economic diction. India's balance-of-payments crisis in 1991 followed an acceleration in economic growth to 5.6 per cent a year.

Low growth rate of 3.5 per cent over three decades and large fiscal deficits fed into current account deficits and depleted foreign exchange reserves, pushed India to the brink of default in 1991.

The general government fiscal deficit (centre and states consolidated) averaged 9 per cent of GDP before the crisis. The overall budget deficit rose from around 7 in 1997-98 to more than 10 per cent in 2002-03, due to a significant increase in government consumption and continued low revenue mobilization.

Persistence of large fiscal deficit resulted in accumulation of domestic debt beyond sustainable levels. The combined domestic debt-to-GDP ratio rose from about 58 in 1985-86 to 85 per cent of GDP in 2002-03 with contingent liabilities from loss-making public enterprises adding another 12 per cent of GDP.

In fact, the domestic debt-to-GDP ratio has accelerated from less than 2 per centage points of GDP per year over the first three years of the 9th Plan period (1997-98 to 1999-00) to more than 4.5 per centage points over the last three years (2000-01 to 2002-03), despite the low interest rates.

Besides this rise in the debt burden, the deteriorating quality of the fiscal stance in the 1990s has been a matter of serious concern for economic managers. Revenues fell considerably during the Ninth Plan period (1997-98 to 2001-02) relative to the second half of the 1980s. Compared with the average for the second half of the 1980s, capital expenditure fell by more than three percentage points of GDP during the Ninth Plan period.

India had no alternative but to seek assistance from the IMF under the Standby Arrangement which it had resisted for too long. In the process, India had to change its development strategy, which they followed for the last 40 years.

The new strategy is a mix of "loose fiscal-tight money" policy that has helped to keep inflation low and prevent worsening public debt dynamics from spilling over into the current account and depleting reserves, as happened in the late 1980s, leading to the 1991 crisis. But this has been at the expense of growth and welfare, as rising interest payments crowded out spending on social and physical infrastructure.

After remaining dormant for four decades, the Indian economy had picked growth momentum in the first half of the 1990s following the policies implemented in response to the 1991 crisis. However, compared with an average growth of around 6 percent through the 1990s, GDP growth decelerated to an average of 5.0 per cent in 1999-2000 and 2000-01 and is now estimated to have further declined to 4.4 per cent in FY2002-03.

There were many factors that have played important roles in depressing Indian economic growth including poor agricultural performance; ill-effects of economic sanctions following the nuclear tests; the hardening of international oil prices from $9.2 per barrel to $37.0 per barrel; meltdown of IT sector; tehelka.com's video-taped revelation about corruption in defence establishment and bankruptcy threats for Unit Trust of India (UTI) the largest mutual fund further eroded investor sentiments; and the persistence of large and unsustainable fiscal deficit (11 percent of GDP) causing public sector debt exceeding 85 percent of GDP. More importantly, the first generation of reforms launched in the early 1990s (after the 1991 balance of payments crisis) appear to have run out of fuel.

The slowdown during the late 1990s was broad-based across sectors, particularly in the agriculture and industry. Agricultural growth slowed to an average of 1.3 percent during last three years from an average of 4.75 percent in the mid-1990s - less than one-third the rate in the mid 1990s - and manufacturing sector growth slowed to an average of 3.8 percent as against 7.5 per cent in the mid 1990s - less than half the rate in the mid 1990s. The slowdown in growth was accompanied by a slowdown in investment, especially in the private sector.

Firms borrowed and invested heavily in the mid-1990s, building capacity for demand from continuing high growth rates and continuing reforms that would have surely generated high returns. Private sector investment growth plummeted to an average of only 3.75 as against an average of 15.2 per cent in the mid 1990s.

Higher public debt and higher interest rates also added to the debt service burden. As a result, resources available for public investment became tighter, with consequences for infrastructure development. The share of public sector investment in GDP declined from 11.2 in 1985-86 to 8.2 in 1992-93 and further to 6.6 per cent in 1997-98, and has now settled at 6.3 per cent of GDP in 2002-03.

The continued deterioration in fiscal balance and the associated rise in public debt along with slowdown in structural reforms are the key factors responsible for the deceleration in growth momentum in India. Given the size and depth of poverty in India, achieving annual growth of 8 per cent per annum is considered necessary to significantly reduce poverty in 5-10 year period.

It is in this context that recent deceleration of growth has emerged as a major source of concern. Notwithstanding the progress in poverty reduction in the past decade, some 400 million people (or 40 per cent of the population) still live on less than $1 a day, compared with 31 percent in Pakistan with same definition.

To look at the overall socio economic conditions of India there are other important criteria as well. More than 2.5 million people sleep on the footpath, and pavement in two major Indian cities only, namely Kolkata and Mumbai.

Anecdote like "millions of poor Indians born and die on footpaths" is not an exaggerated statement indeed. According to the WHO Report India is the second most AIDS-affected country in the world after South Africa, where up to 5 per cent of the population is already AIDS-infected or highly vulnerable to that fatal disease.

According to a recent statement of Indian Home Minister presently 165 separatist groups are actively engaged in secessionist activities in the nook and corner of the country, including 107 groups in the resources rich north eastern provinces. Communal violence's are on the rise. Minorities including Muslims, Christians and Untouchables are frequently subjected to arson and killings and wanton destruction of their property.

Violence and social disharmony, if not controlled may eat up whatever India has gain in her economic sector in the last few years. A comparison of economic performance of Pakistan and India during the outgoing fiscal year 2002-03 reveals interesting facts. [See Table-1]. It is evident that Pakistan is far better placed and reached a position of macroeconomic stability in recent years.

The fiscal space after long journey of fiscal prudence has finally attained and Pakistan can accelerate pace of social economic development faster than any other country in the region including India. Pakistan's per capita income has already increased from $420 in 2001 to $492 in 2003.

Pakistan has already achieved primary fiscal surplus and revenue deficit is near elimination which has helped Pakistan to improve its debt dynamics.

On the other hand the sharp increase in revenue deficits, which doubled from less than 3 per cent in the late 1980s to more than 6 per cent of GDP over the past six years, is a matter of serious concern for Indian economic managers.

Falling revenues-and rising expenditures have crowded out development spending, with negative implications for long-run growth and welfare. Growing interest payments have crowded out public investment, and high real interest rates have constrained private investment. Even though interest rates have declined over the past 18 months, public debt dynamics have continued to worsen.

Pakistan's exports are growing at a faster pace than India. Revenue collection in Pakistan has substantially improved during last three years while in India these are deteriorating. On the other hand Pakistan has not only succeeded in arresting increasing debt burden but domestic debt to GDP ratio has improved from 52.6 in 1999-2000 to 4 per cent in 2002-03.

This is because of the fact that Pakistan is able to lower fiscal deficit at around 4.5 per cent in 2002-03 while fiscal deficit in India has risen to double digit at 11 per cent of GDP. There was an across-the-board deterioration of fiscal indicators during the 9th Plan relative to the second half of the 1980s and an even more striking deterioration is to follow in the years to come. Table-1:

Many intellectuals in Pakistan are impressed with the impressive growth performance of India during 1990s but they must look into quality of growth. Pakistan had higher economic growth in the 1980s but fiscal deficit was left unbridled which had given rise to serious macroeconomic crisis in the 1990s.

Same is happening in India where fiscal stimulus is seen as desirable to counter the slowdown in private sector activity. But the arguments for a fiscal stimulus is not convincing when public debt levels are rising at such a brisk pace.

India's large fiscal imbalances pose a serious threat to sustained growth and development over the medium term. The persistence of current fiscal trends will, at best, limit growth and job creation. And slower growth would, in turn, speed the deterioration in debt dynamics.

If this negative cycle continues, a full-fledged fiscal crisis cannot be ruled out. On the surface, these fiscal indicators are worse than those faced in 1991-and worse than in many other countries that actually suffered a macroeconomic crisis. But the risk of crisis in India today is mitigated by the country's strong foreign exchange reserves. These reserves are able to finance 11 months of imports while Pakistan maintains reserve level of sufficiency for 12 months imports.

India has added about $22 billion during the past fiscal year, about 40 per cent of it after November 2002. An unknown part of this might have been driven by capital inflows related to fears of the Iraq war, so "this pace might not be maintained" (Reserve Bank of India 2003 report).

Without a fiscal adjustment, the growth even at 8 percent would be substandard. In other words, growth could continue to be substandard even if a crisis does not erupt-and avoiding crisis is not enough for India in present fiscal situation.

Major challenges for India in the near term are; first generation reform running out of fuel, fiscal responsibility and budget restraint law, continuing regional tension, communal violence, unsustainable fiscal deficit, growing subsidy and contingent liabilities, rising public debt, crowing out of private sector, economic growth slowing, likely setback on poverty front.

Table-1: Pakistan and India

A comparison of economic performance of 2002-03

Pakistan India

Real GDP growth (%) 5.1 4.3

Industrial growth (%) 8.6 5.8

Inflation (% growth in CPI) 3.1 4.0

Revenue (% of GDP) 17.6 18.4

Expenditure (% of GDP) 22.2 28.8

Fiscal deficit (% of GDP) 4.6 10.4

Revenue deficit (% of GDP) 0.5 6.9

Primary balance (% of GDP) 0.4 -3.8

Current account deficit (% of GDP) 4.8 0.7

Domestic debt (% of GDP) 46.0 85.0

Export growth (%) 22.0 19.2

Link:

http://www.dawn.com/2003/11/03/ebr11.htm

Comment